Understand VAT Ireland cross-border transactions, input deduction traps, reverse charges, and B2B/B2C scenarios for business compliance.

Understanding Ireland's VAT Rates

For businesses dealing in cross-border transactions, understanding Ireland's VAT rates is crucial for compliance. The standard VAT rate in Ireland is 23%, which applies to a broad array of goods and services, including electronics, professional services, and clothing. A reduced rate of 13.5% covers construction services, energy supplies, and certain maintenance services, reflecting the government's aim to alleviate the tax burden on essential goods. Meanwhile, a 9% rate supports the tourism and hospitality sectors, covering items like newspapers and some digital content.

The zero rate, while technically subject to VAT, allows businesses to claim input VAT on related purchases, which is significant for exporters of goods from Ireland and suppliers of most foodstuffs and children's clothing. Misunderstanding these rates can lead to incorrect invoicing and VAT returns, especially in cross-border dealings where different rates might apply in the destination country. Familiarity with these nuanced rates ensures that businesses can avoid costly errors.

For instance, a UK-based e-commerce company selling digital products in Ireland must apply the correct VAT rate depending on the product type. Misapplying a standard rate when a reduced or zero rate is applicable can lead to overpayment of VAT or penalties in case of underpayment. Consequently, comprehensive knowledge of Ireland's VAT rates is non-negotiable for businesses engaged in cross-border transactions.

Navigating Input VAT Deduction Traps

One of the more challenging aspects of VAT compliance in Ireland is navigating input VAT deduction. Businesses often fall afoul of regulations by claiming input VAT on non-deductible expenditures, leading to potential penalties. Common traps include VAT on petrol, which is entirely non-deductible, and entertainment expenses, such as client meals and corporate events, where VAT cannot be reclaimed even if the expense is allowable for other tax purposes.

- Petrol: No VAT deduction is allowed, regardless of usage. Diesel, however, permits a partial deduction.

- Entertainment: No VAT recovery, even if justified for other taxes.

- Passenger Vehicles: Generally non-deductible, except for specific trades like taxi services.

Understanding these nuances is vital for businesses. For instance, a company purchasing a fleet of cars for employee use may face a significant non-recoverable VAT cost unless they primarily operate in a sector with special allowances. Thus, strategising purchases and understanding these rules can prevent unexpected financial burdens.

The Reverse Charge Mechanism Explained

The reverse charge mechanism is an essential tool for businesses receiving services from non-Irish suppliers. It applies when an Irish business purchases services such as digital advertising from companies like Google or consultancy services from a UK-based firm. Essentially, the Irish business must account for VAT as if it supplied and received the service itself, which involves charging itself VAT and simultaneously claiming it as input VAT.

This process ensures that Irish businesses purchasing from non-EU suppliers do not face competitive disadvantages. While often resulting in a net zero VAT impact due to offsetting, the compliance aspect is critical. Failure to correctly apply the reverse charge can result in audits and penalties. It's crucial for businesses to ensure their accounting systems are set up to handle these transactions smoothly.

For example, a tech startup in Dublin might engage a US-based software provider. The startup would need to self-account for the VAT on these services to remain compliant. Properly applying the reverse charge mechanism can prevent operational disruptions and financial penalties, making it a fundamental practice for businesses engaged in significant cross-border service procurement.

Cross-Border B2B Transactions: Key Considerations

Cross-border B2B transactions present unique VAT challenges that can affect cash flow and compliance. When Irish businesses sell to VAT-registered entities in other EU countries, they can generally zero-rate the sale, provided they obtain and verify the buyer's VAT number. This requires meticulous record-keeping and timely communication with customers to ensure compliance.

However, if the buyer is not VAT-registered, the situation changes. Here, the seller might have to charge Irish VAT, complicating invoicing and accounting processes. Hence, understanding the VAT status of clients abroad is crucial for Irish businesses to correctly apply VAT and avoid negative financial implications.

- Verify customer's VAT number: Essential for zero-rating sales.

- Maintain thorough documentation: Ensure compliance and ease of cross-border audits.

- Adapt invoicing systems: To handle VAT correctly in diverse situations.

For instance, an Irish manufacturer exporting goods to a German company must confirm the company's VAT registration to correctly zero-rate the transaction. Failing to do so could result in VAT being charged incorrectly, thus affecting the competitiveness of the offering and potentially leading to penalties.

Cross-Border B2C Scenarios: Different Rules Apply

When dealing with cross-border B2C transactions, Irish businesses face different VAT challenges compared to B2B transactions. For sales to non-business customers in other EU countries, the VAT rules are dictated by the country where the customer is located. This can mean that businesses must register for VAT in those countries once their sales exceed certain thresholds, which varies by country.

This requirement can complicate operations, particularly for smaller businesses without the resources to manage multiple VAT registrations. The introduction of the One-Stop Shop (OSS) scheme by the EU helps mitigate this by allowing businesses to account for VAT on sales to consumers across the EU through a single VAT return.

Consider a small Irish retailer selling handmade goods online to French consumers. As sales grow, the retailer may surpass the French VAT threshold, necessitating VAT registration in France. By using the OSS scheme, they can streamline compliance by consolidating their EU VAT obligations, thus reducing administrative burdens and allowing them to focus on business growth.

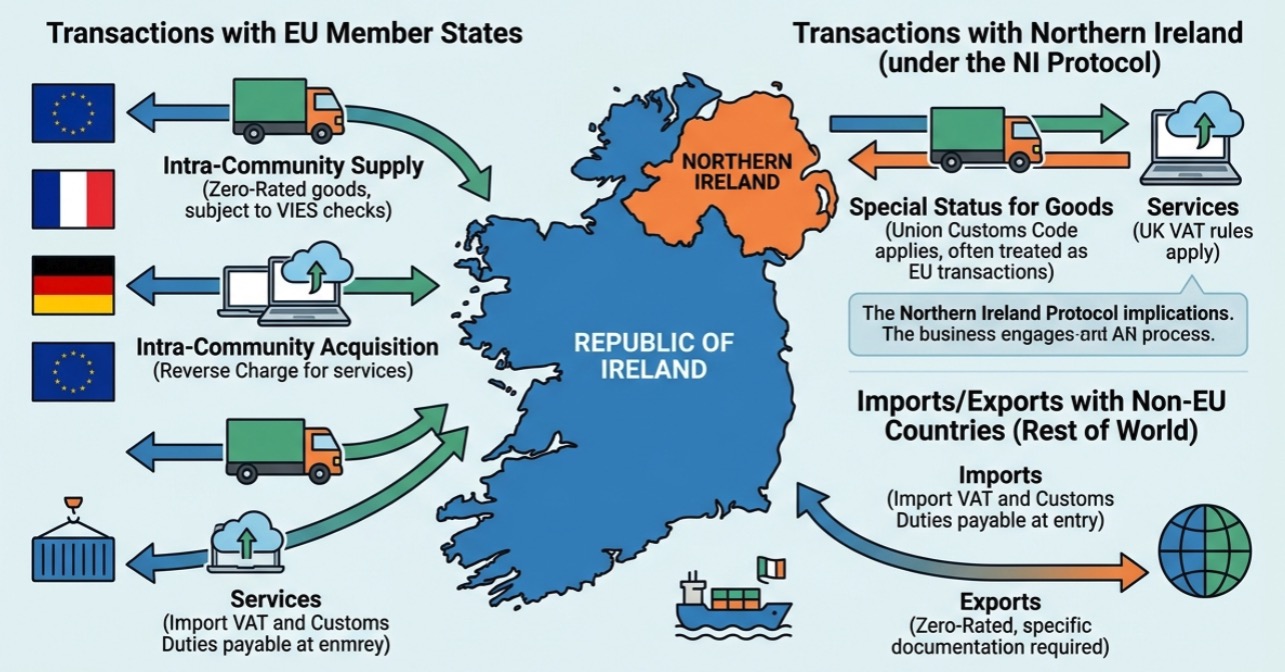

The Impact of Brexit on VAT Transactions

Brexit has introduced complexities into VAT transactions between Ireland and the UK, affecting both imports and exports. The UK is now treated as a non-EU country, meaning Irish businesses need to adapt to new customs procedures and VAT rules. For exports to the UK, Irish companies can zero-rate the sale, but must contend with UK import VAT and customs declarations on goods entering the UK.

Conversely, importing from the UK into Ireland requires Irish businesses to pay import VAT, though this is typically reclaimable in their VAT returns. This change mandates a re-evaluation of supply chains and logistics, as businesses must now manage increased administrative tasks and potential cash flow impacts due to import VAT.

- Customs declarations: Necessary for all goods moving between Ireland and the UK.

- Zero-rating exports: Applies to goods sold to UK businesses but requires proof of export.

- Import VAT: Payable on imports from the UK but reclaimable.

For instance, an Irish distributor importing UK-manufactured electronics must now handle customs declarations and pay import VAT, influencing pricing strategies and cash flow management. Adapting to these changes is essential for maintaining operational efficiency and regulatory compliance post-Brexit.

Practical Tips for Managing VAT Compliance

Effective VAT management is critical for businesses engaged in cross-border transactions to avoid penalties and optimise financial outcomes. Implementing robust accounting systems that automatically calculate VAT and reverse charge where applicable can significantly reduce errors. Regular training for finance staff on current VAT rules ensures that your team remains compliant with the latest regulations.

Consulting with VAT specialists can provide tailored advice, especially when dealing with complex transactions or when entering new markets. Additionally, leveraging technology such as VAT compliance software can streamline processes and provide real-time insights into VAT liabilities across different jurisdictions.

For example, a multinational operating in Ireland might face intricate VAT compliance requirements across different countries. By engaging a VAT consultancy and implementing advanced accounting software, they can centralise and simplify their VAT management, thus allowing them to focus on strategic growth rather than administrative challenges. In the dynamic landscape of cross-border business, proactive VAT management is not just a compliance requirement but a competitive advantage.

About Peterson Family Office

Peterson Family Office Limited was established in Dublin in 2022, serving high-net-worth international families with a focus on education pathway planning, tax advisory, and long-term family strategy. Our philosophy — Professional · Disciplined · Long-term Commitment — guides every aspect of our work. We combine deep knowledge of the Irish and European landscape with a genuine understanding of the needs of families relocating from Asia and beyond.

Our three core service areas — Education Pathway Planning, the 1+1 Dual Mentorship System, and Family Office Services — work together to support families at every stage of their journey in Ireland. To learn more about how we can help your family, visit About Peterson Family Office.

Related Articles

Deductions Available for Property Rental Income in Ireland

Explore tax deductions on property rental income in Ireland, benefiting high-net-worth families with informed tax strategies.

Navigating Crypto Tax Obligations for Investors in Ireland

Explore crypto tax obligations in Ireland for high-net-worth families investing in digital currencies.

Capital Gains Tax on Cryptocurrency in Ireland: A Guide

Explore how capital gains tax affects cryptocurrency transactions for high-net-worth families in Ireland.